This article reflects the opinion and analysis as well as information collated by AE Research Management Sdn Bhd, and does not constitute an investment advice or recommendation

Penetration of SiC in the power semiconductor space will accelerate in the coming decade, as power management ICs made on SiC (silicon carbide) substrates have lower current leakage (hence higher efficiency) than silicon-type, and can operate at higher voltages and switching frequencies.

The rapid and lumpy capacity built-out by SiC power device players in the past 2-3 years have led to intense price pressure. Together with the burden of the depreciation charges on these new facilities, the operating losses at SiC business of key players such as ROHM appeared alarming. Not helping is the slower than expected sales of EVs (electric vehicles), a major user of SiC power chips.

To a large extent, the lumpy capacity additions (and the resultant near-term excess capacity) is inevitable. As SiC is a new technology at nascent stage of taking off, expansions by any player have to be greenfield in nature, ie it is not possible to just go for incremental line expansions unlike in matured sector.

Notwithstanding the current excess capacity and pricing pressure, the underlying state of competition is that SiC power device industry is not fragmented at all. According to data from TrendForce, the top 5 suppliers – ST Microelectronics, Onsemi, Infineon, Wolfspeed and ROHM – account for over 90% of sales. This is almost as concentrated as the case of semiconductor memory market.

Similar supplier concentration exists in the market for SiC substrates (the wafers used to make SiC power devices). Pricing pressure has been even more intense than the device market due to presence of two large China substrate suppliers. Like Wolfspeed, ROHM is also a merchant supplier of SiC substrates to other fellow device makers such as to ST Microelectronics.

Capacity Expansion Will Be Better Controlled Going Forward

The good news is that all greenfield plants are now completed and further expansion can be better controlled from now on.

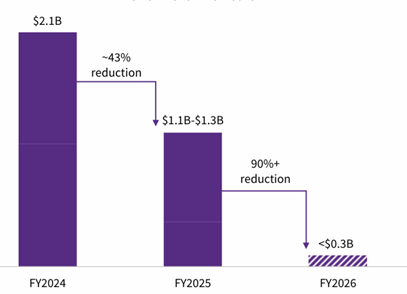

In fact, key player Wolfspeed (USA) is so financially constrained that the company is reducing capex by almost 90% to mere basic maintenance level (chart 1).

Chart 1: Capital Expenditure at Wolfspeed

Source: Wolfspeed

The capex at other main players are also falling substantially, including at ROHM where spending was down by 55% in FY26/3 from the peak of 2 years prior. And smaller aspirants such as Renesas and Qorvo have totally abandoned their plans.

SiC Adoption – An Irreversible Megatrend

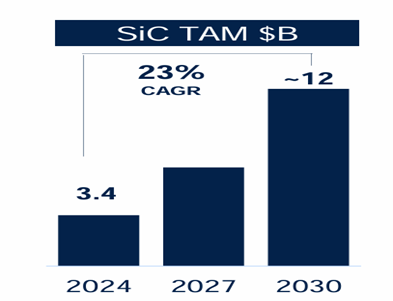

On the demand side, the long-term forecast for SiC devices is for growth rate of 20-30% p.a., reaching some USD 12bn per annum by 2030 (chart 2). SiC devices are more suited for higher voltages and switching frequencies, compared to the conventional silicon devices.

Chart 2 – Rapid Growth in Total Addressable Market

Source: Omdia, Yole, ST Microelectronics

The growth outlook is often associated with the rapid take off in EVs globally. Indeed, rising adoption of SiC power devices in EVs is a megatrend. Nonetheless, the applications are much more broad-based than just for automotives. New attractive markets are also emerging, in particular in power management at AI data centers which increasingly require to operate at a much higher voltage for efficiency (less heat/energy loss).

AI data centers were probably not featured prominently in SiC TAM (total addressable market) calculation when the investment decision of many greenfield fabs were made circa 2019-2020. As it stands, last year alone some 10GW of new AI data centers capacity commenced construction. These new capacity starts will entail some 333,000 server racks (each rack estimated to be 30kW), and each rack is likely to require some USD 12,000 worth of power semiconductors. Hence, total power semiconductors demand from AI data centers alone is approximately USD 4bn per annum and rising rapidly.

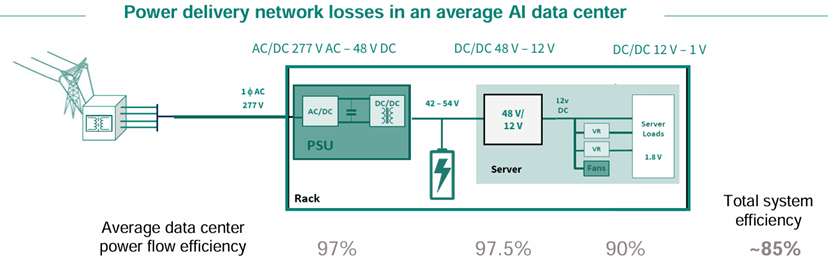

Chart 3: Low Power Efficiency at AI Data Centers

Source: Infineon

Granted not all the power semiconductors required will be SiC-based. However, in order to increase power efficiency (from the current lowish 85%), the data centers will have to use a higher proportion of SiC-based chips, especially as operating voltages are raised to minimize energy losses (high voltage imply a lower current, thus less resistive losses for example).

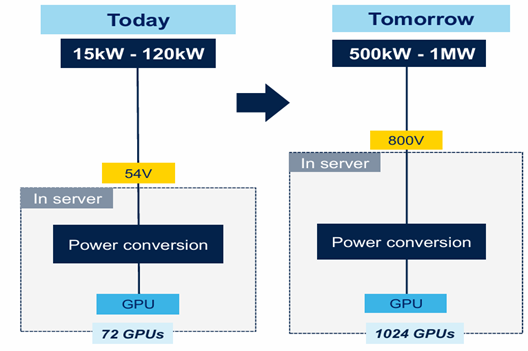

Chart 4: Towards Much Higher Operating Voltages at Data Centers

Source: ST Microelectronics

Another major addressable market for SiC devices, which could even exceed that of data centers, is in the power grid infrastructure. Similarly, to minimize transmission and conversion losses, the operating voltage is raised and adoption of solid-state transformers will become common.

All these structural shifts will support demand for more SiC power semiconductors.